Accelerating Net Zero Chemical Manufacturing Series: Which feedstocks will we be using to produce chemicals in 2050?

In our first article in this series, we explored how investment in low carbon energy, carbon capture and storage (CCS) and low carbon hydrogen infrastructure will be critical to enabling Net Zero chemical manufacturing by 2050.

In this next article, we explore which feedstocks will we be using to produce organic chemicals in 2050, and where do we have the capability in the UK to develop the key process technologies that will be required to convert alternative feedstocks into chemical products?

At the moment approximately 90% of organic chemicals are produced from crude oil, the rest from non-fossil feedstocks like biomass, this is likely to change as the UK moves towards net-zero carbon emissions and a more circular economy, but how?

No-one can provide a definite answer, but two very extreme scenarios are presented below:

1. Crude oil remains favoured feedstock for chemical production

Currently, most crude oil is used for the production of fuels with less than 20 % being refined for petrochemical markets. As the demand for fuels reduces (due to electrification and the development of sustainable alternatives) the crude oil price will result in favourable economics for the production of chemicals. This scenario would mean we can continue to utilise our existing petrochemical refining infrastructure and downstream chemical processing assets.

2. Alternative (non-fossil) feedstocks are favoured for chemical production

The value of carbon embedded in every product is recognised, reflected in policy and economics, creating value in a circular economy for all chemicals and materials containing carbon. Under this scenario, non-fossil feedstocks, like ‘waste’ carbon dioxide (CO2) from industrial processes, as well as other gas streams (biogas, syngas) and other solid wastes (plastic, biomass, municipal waste), become a favourable feedstock.

Some of these carbon-containing feedstocks are combusted to satisfy local energy demand and some are transformed into low-carbon fuels but a significant proportion is utilised to produce chemicals and materials, displacing virgin-fossil derived carbon and creating a circular loop for carbon. Some of these ‘waste’ carbon feedstocks are recycled via repurposed petrochemical refining assets and go on through the existing downstream chemical supply chain. The rest is processed in new biorefineries and through other new chemical or industrial biotechnology processes, creating new value chains for the downstream chemical supply chain.

It is unclear which of these scenarios is more likely at the moment. We certainly do not see the petrochemical tap being turned off any time soon. It will depend on UK and global policy and ultimately is likely to be a mix of both. It is worth noting that the UK Petroleum Industry Association (UKPIA) Vision for the Future suggests that traditional refineries will predominantly be producing low carbon fuels (for aviation and marine) utilising a range of non-fossil feedstocks in the future and for downstream petrochemicals it expects that the development of circular economy principles will reduce demand for petrochemical feedstocks by 2040-2050.

The Chemistry & Industrial Biotechnology Team believe that given the current policy messages around Net Zero and the drive towards a more Circular Economy, there is a need to act now to develop new value chains for chemicals from alternative feedstocks so that we can lead in Net Zero chemical manufacturing.

So where are our strengths in capability for developing these chemical feedstocks of the future?

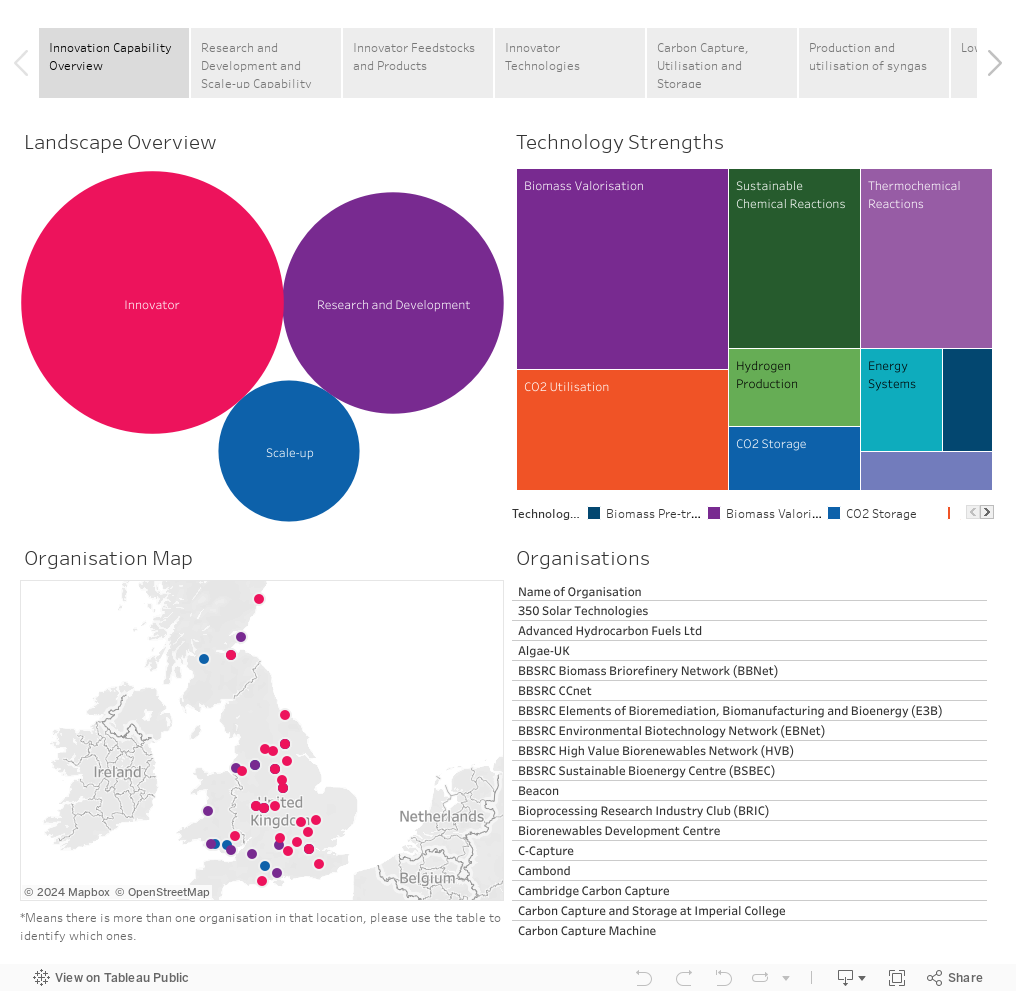

In order to better understand the UK opportunity, we have undertaken a project to analyse our capabilities – across the research base, in scale-up, and our innovator community – for developing the process technologies that will be needed to produce chemicals from alternative feedstocks in a Net Zero world by 2050.*

Through this activity, we have identified 38 academic centres of excellence, networks and hubs and Research & Training Organisations (RTOs) that have core capabilities in the core technology areas identified as key for developing alternative feedstocks-to-chemicals. Ten of these organisations have access to pilot-scale facilities. In addition, we have identified 46 innovators (SMEs, start-ups) who are actively developing key process technologies, or key enabling technologies, that could play a role in enabling the manufacture of chemicals from alternative feedstocks. We have analysed these organisations considering their technology strengths, feedstock type, products and locations. Browse the output of our analysis in the data map below.

Based on our analysis, we see capability strengths and opportunities in a few key pathways, but in particular the first two:

- Carbon Capture and Utilisation in combination with hydrogen

- Syngas as a vector to produce chemicals

- Upgrading of low-carbon fuels into low-carbon chemicals

- Biomass valorisation

- Valorisation of waste plastic

So what’s next? How do we develop these opportunities?

As a first step, we would like you to review our Capability Maps and tell us what we are missing. We will be writing more detailed articles on each of these opportunities over the coming months and inviting you to contribute to workshops to help build innovative projects in these areas. The goal here is to stimulate investment or funding, so keep an eye out for notices of new events in forthcoming newsletters.

But hold on, my technology/organisation is missing from the Capability Maps?

We have populated this Capability Map based on our current knowledge & network, focusing on the process technologies that we think are going to be critical in a Net Zero world. We appreciate that we haven’t covered all technologies. For instance, chemical recycling of critical raw materials will be incredibly important as we become ever more reliant on these materials for our energy needs. We have also not undertaken an in-depth analysis of all that can be offered through industrial biotechnology and synthetic biology processes, nor have we gone into detail on all of the different combinations of process technologies (continuous flow, spinning disk reactors, photochemistry, electrochemistry) that could help reduce the overall energy use and environmental impact associated with making chemicals. All of these technologies and processes will have an important role to play!

We have also kept our map of academic capability focused on centres of excellence, networks and hubs only, rather than individual researchers or research groups. If you think we have missed your organisation or missed a key technology, we want to hear from you! Please contact Dr Sheena Hindocha or Dr Peter Clark.

* This activity has been undertaken as part of a project sponsored by our partner Innovate UK and in response to Activity 5B of the Chemical Sector Energy Efficiency & Decarbonisation Action Plan which was to “map existing UK research expertise, centres and areas of strength in relation to innovation development and scale-up relevant to the key decarbonisation technologies identified in the innovation mapping work”

** This analysis was informed by a desktop assessment of key centres of academic excellence, academic hubs & key academic networks, RTOs and innovators within our network. We also interviewed individuals at 14 experts from academia and RTOs to gain a more in-depth understanding of their expertise. We also ran a competition to identify Top Innovators in this area, allowing us to better understand their innovation challenges and capabilities.

Related Content

Related programmes

Chemicals Innovation Landscape

Connecting the UK’s growing Chemicals industry with industrial collaborators, research-based expertise, investment opportunities and funders.

Net Zero Chemicals Landscape

Connecting the UK’s growing Chemicals community with industrial collaborators, research-base expertise, investment opportunities and funders.